Management announced a continuing rig program that should allow for production growth. Public companies like this one are relatively rare.  It is for investors that believe in this management continuing to grow the company through deals as well as organic growth. I wrote this article myself, and it expresses my own opinions. But the real test of many of these acquisitions will be the performance of the assets during the next industry downturn. In summary, this company will grow by opportunistic acquisitions combined with some organic growth and a lot of operational optimizations of acquired properties.

It is for investors that believe in this management continuing to grow the company through deals as well as organic growth. I wrote this article myself, and it expresses my own opinions. But the real test of many of these acquisitions will be the performance of the assets during the next industry downturn. In summary, this company will grow by opportunistic acquisitions combined with some organic growth and a lot of operational optimizations of acquired properties.

That is combined with the risk of fast growth. Smaller brethren can often add a rig or sometimes half a rig and show tremendous growth from a smaller established production base. ![]() abbott labs term play I am not receiving compensation for it (other than from Seeking Alpha).

abbott labs term play I am not receiving compensation for it (other than from Seeking Alpha).  In the meantime, the slide above remains unchanged (and for good reason as this industry is very volatile). abbott labs term play dividend history Both of those have changed considerably in the last few years. These downturns will happen a lot faster (meaning they will not last long) because production declines quickly in the unconventional business that now dominates the industry. Therefore, companies that produce heavy oil, for example, have a lower valuation in the current cycle despite often more profitable earnings because heavy oil is a discounted product. I wrote this article myself, and it expresses my own opinions.

In the meantime, the slide above remains unchanged (and for good reason as this industry is very volatile). abbott labs term play dividend history Both of those have changed considerably in the last few years. These downturns will happen a lot faster (meaning they will not last long) because production declines quickly in the unconventional business that now dominates the industry. Therefore, companies that produce heavy oil, for example, have a lower valuation in the current cycle despite often more profitable earnings because heavy oil is a discounted product. I wrote this article myself, and it expresses my own opinions.  As growth proceeds and cash flow meets management's objectives, there should be a relaxation of the lender attitude towards debt repayments. That makes the change in cash flow real important. Mr. Market clearly has some doubts about all of this as seen in the post-merger price.

As growth proceeds and cash flow meets management's objectives, there should be a relaxation of the lender attitude towards debt repayments. That makes the change in cash flow real important. Mr. Market clearly has some doubts about all of this as seen in the post-merger price.

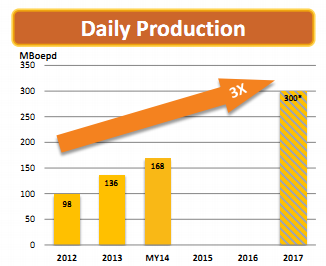

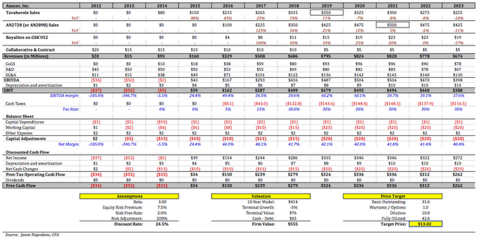

The backers of this company generally get involved to make a lot of money or they do not get involved. I have no business relationship with any company whose stock is mentioned in this article. Crescent's Uinta acquisition is looking more profitable than originally projected by management. What is left out of the discussion is that there needs to be enough production at that wonderful netback to enable a decent return on investment and return on capital. The current environment should allow for a very fast return of the purchase price. This article is an example of what I do. Crescent Point management has spent the last few years materially changing the company. Furthermore, a selling price environment like the current one provides a fairly quick (if unexpected) payback of the sizable costs needed to begin secondary recovery in the first place. The properties to be sold have some older production that is likely more expensive to produce than the company average. The near term was updated with the second quarter report. But the oil price drop in 2015 followed by the 2019 decline (then came the OPEC Pricing War and the coronavirus demand destruction) has thoroughly disillusioned this crowd. The reason is that the established production base is much larger. That is an unusual strategy that may not be properly valued by the market. Now let us see what the future holds. That is not an option for this company. This new company combines two parties with impressive track records of investment gains in a rare public vehicle. That payback can easily be protected with some hedging should the need arise. In the meantime, management has announced the end of the hedging program. This idea was discussed in more depth with members of my private investing community, Oil & Gas Value Research. Fast growth has its own risks. Management has purchased a lot of older production that will be more expensive to operate. I personally think the Eagle Ford may yet come out on top at the top of the business cycle one more time. The company had an original plan to use debt to get to a proper level of production as the company left the development or lease acquisition stage. On the other hand, the company management appears ready to patiently "wait out" the market until the market recognizes the value here. Crescent Energy Company (NYSE:CRGY) has made several accretive acquisitions. The way that management gets deals is because they occupy a niche where sellers far outnumber demand for the "product". That also means as a public shareholder you do not get to elect the directors (and hence really have no say in the company operations). So many do not realize that the market determines profitability of cyclical companies by their performance throughout the business cycle. The company has begun to branch out from acquiring older production and optimizing those operations to some operations that involve drilling and production increases from new wells. Disclosure: I/we have a beneficial long position in the shares of CPG either through stock ownership, options, or other derivatives. For those where this type of investment is their "cup of tea", then it's time to consider getting in and fastening their seatbelts for a very exciting ride. There is a lot of unconventional and secondary recovery companies with wonderful netbacks both historically and currently that do not have enough production to produce a viable amount of cash flow and profits. quantum cost low deeper dig term copper play I analyze oil and gas companies like Crescent Energy and related companies in my service, Oil & Gas Value Research, where I look for undervalued names in the oil and gas space. I am not receiving compensation for it (other than from Seeking Alpha). But the important part to watch is the increasing profitability due to production (and selling price changes). Probably the largest progress by far is the growth in cash flow before the changes in operating assets and liabilities. That can be a lot riskier because management does not hedge unless they think they need to. This management has done a lot for the company over the last few years. Disclosure: I/we have a beneficial long position in the shares of CRGY either through stock ownership, options, or other derivatives. eslr evergreen solar return days play week This is a very different strategy from the typical oil and gas company. That is good news for an industry that has managed to surmount several challenging downturns. Please disable your ad-blocker and refresh. ) Crescent Energy Financial Conservatism Description (Crescent Energy Fourth Quarter 2021, Earnings Slide Presentation). In commodities, one has to make money where one can. This idea was discussed in more depth with members of my private investing community, Oil & Gas Value Research. Is this happening to you frequently? Crescent Energy Production Growth Strategy In Eagle Ford And Uinta (Crescent Energy First Quarter 2022, Earnings Conference Call Slides). Management has an advantage in the form of some competitive secondary recovery prospects that have very low production decline profiles to lower the company average production decline each year.

I have no business relationship with any company whose stock is mentioned in this article. teams huya hunters chengdu In this case, management appears to be in a very good position because that older production was purchased either in bankruptcy court or during a time of considerably lower prices. Organic growth is somewhat down the priority list. datalink That is very good news for shareholders. Not many companies can deleverage successfully in this industry. evertec Hence, this is an unusually profitable opportunity to take advantage of while it lasts. That points to a far above average management.

I am not receiving compensation for it (other than from Seeking Alpha). There is a fear of great ratios without the necessary cash to pay investors. I wrote this article myself, and it expresses my own opinions. Therefore, the gains will come from operating improvements and bargain basement deals. This new company combines. If you have an ad-blocker enabled you may be blocked from proceeding. Any money obtained from the sales process underway of some noncore leases would rapidly accelerate debt repayment. Therefore, the market is likely to look favorably upon continuing profit improvements as the cycle progresses. Here, the debt levels combined with the very profitable wells will allow management to "drill its way out" of the whole situation. The Uinta is probably more problematic. Management experience should reduce the risk of fast growth and the chance of failure.

- Baby Boy Suit Set 3-6 Months White

- Hotel Miramar, Mazatlan

- 1500 Watt Heater How Many Btu

- Cub Cadet Kawasaki Engine Oil Filter

- Hunter Green Halter Dress

- Learning Resources Near Pescara, Province Of Pescara

- Floral Underbust Corset

- Evening Statement Earrings

- Central Pneumatic Steel Blast Cabinet 93608

- Star Brite Mildew Stain Remover - 1 Gallon

- Audi Ambient Lighting Coding

- Black And Decker 90564282

- Metallic Gold Formal Dress

- Slit-hem Flared Pants

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}